The Optimal Use of Debt in a SaaS Business

A Guest Post by:

A Guest Post by:

Todd Gardner

SaaS Advisor Ltd.

Todd is an innovative advisor to SaaS companies on growth strategies.

Until a few years ago when the SaaS lending space really took off, there were very few options for a SaaS company to fund its growth with debt. Now, however, a quick google search will yield dozens of lenders focused specifically on SaaS. How do companies decide what credit offering is right for them?

SaaS Borrowing is Unique

The first thing to understand is that SaaS borrowing is different than other types of commercial borrowing. SaaS companies borrow money for one reason — to extend their runway. Extending the runway allows MRR to grow and create enterprise value without raising additional equity and diluting shareholders. Debt is being used instead of equity to support operating losses.

In traditional borrowing, the structures have been well defined for years: accounts receivable and inventory lines fund short-term working capital, and term loans fund the purchase of equipment, buildings, or other companies. With only slight nuances in the structure available, selecting a lender primarily came down to the lowest interest rate or a personal relationship.

It’s All About Runway

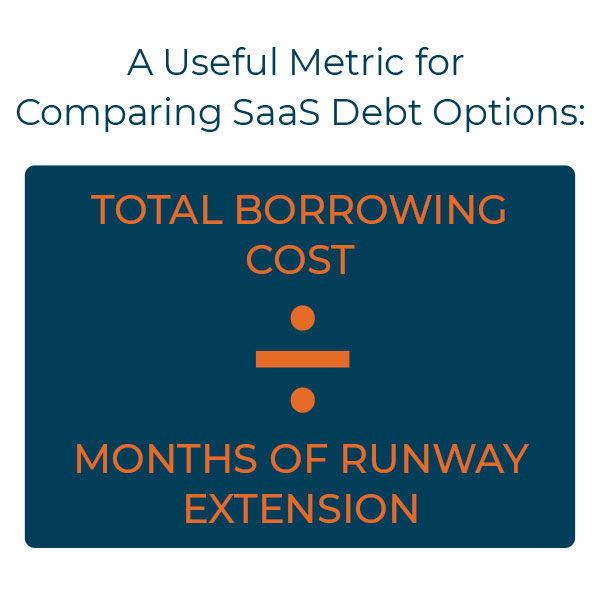

With a SaaS business, however, selecting a lender should come down to understanding how long each approach extends the company’s runway. Once that is known, the loan’s total cost can be divided by the number of months of the runway extension.

This is a good metric to use to compare debt options. This is not perfect, but useful.

Model It

To effectively understand runway extension, borrowers must create a monthly “most likely case” financial model covering at least the next 36 months. Holding the operating plan assumptions constant, model how the different loan structures extend the company’s runway. This is the only way to determine the best loan option, and it also provides direct insight into which specific terms of the loan impact the runway the most.

The basic key drivers of runway extension for a single loan are relatively obvious:

- the loan amount

- the interest-only period duration

- the overall amortization

For a credit facility, the basic drivers are:

- the length of the commitment

- the maximum amount of the facility

- the advance formula (if there is one)

- the structure of the individual draws

Modeling a credit facility is a little more complex than a single loan but certainly doable. Make the model as simple as possible, keeping in mind that the base assumptions about the underlying business are all estimates, so over-engineering the credit facility part of the model will not improve its accuracy.

Covenants

Apart from the basic items listed above, financial covenants are the other big driver of the runway extension. Having no covenants is best, obviously. That said, most borrowers can reasonably project and negotiate operating covenants like churn and profitability in a way that will not constrain their growth or risk a covenant violation. Be mindful of overly restrictive profit covenants, however, as they can limit the business’ ability to actually use the cash it’s borrowing. It also makes sense to avoid any covenants tied to new bookings, which can be volatile and hard to predict.

Balance sheet covenants such as a quick ratio, current ratio, or minimum cash balance should be avoided entirely and are likely to shorten the runway significantly. More often than not, these covenants require the business to carry a significant amount of cash on the balance sheet and result in the company being unable to use much of the cash it has borrowed.

When to Borrow

A common practice of many SaaS lenders is to lend money, typically a term loan, to companies that have just raised a round of equity. This is great for the lender, but it is least effective at extending the businesses’ incremental runway beyond what it otherwise would have been. Most of the debt will be repaid by the time the company would have run out of cash from the equity round. If a company does decide to borrow money concurrent with or soon after an equity round, make sure the interest only period and amortization period are as long as possible.

Subordinated Debt

Sub-debt is most effective when structured as a term loan with a long interest-only period. Keep in mind, however, there are significant transactional, legal, and administrative costs involved in having more than one lender. Typically, a borrower needs to be borrowing somewhere above $5 million in total debt for sub-debt to be helpful in terms of extra leverage.

Alternative Structures

With the rise of many different lenders targeting SaaS, some truly unique structures have emerged. Regardless of what is claimed by the capital provider, however, it is important to remember they will get paid back, plus profit, one way or the other. This is why modeling is so important. The actual cost of some of these programs, particularly those with repayments tied to revenue, is hard to estimate without a financial model. Also, keep in mind that financing alternatives that reduce the amount of revenue that would otherwise be recognized will not show a cost on the P&L, but by lowering MRR, they have an outsized cost on the company’s valuation. Factoring is one financing method that can lower revenue, and so are discounts to customers to pre-pay their subscriptions.

Conclusions and Recommendations

The use of debt in a SaaS businesses (excluding M&A financing) is all about supporting growth investments that would otherwise have been funded by equity, or not made at all. In a healthy growing SaaS business, a good proxy for growth is runway extension, so the benefit of any debt financing is the length of the runway extension it supports.

Generally speaking, credit facilities that scale automatically with MRR and are committed for multiple years are the most effective borrowing structure to extend a SaaS company’s operating runway. They also have the benefit of allowing the borrower to draw down capital only as needed and thereby reduce total interest expense. Alternatively, large term loans with multi-year interest-only periods and at least 3 or 4 years before maturity are also good structures for extending runways. This is particularly true if they are used when the business is already low on cash.

Subscribe and Stay Informed

Sign up today to read our newsletter for helpful information